Market Overview:

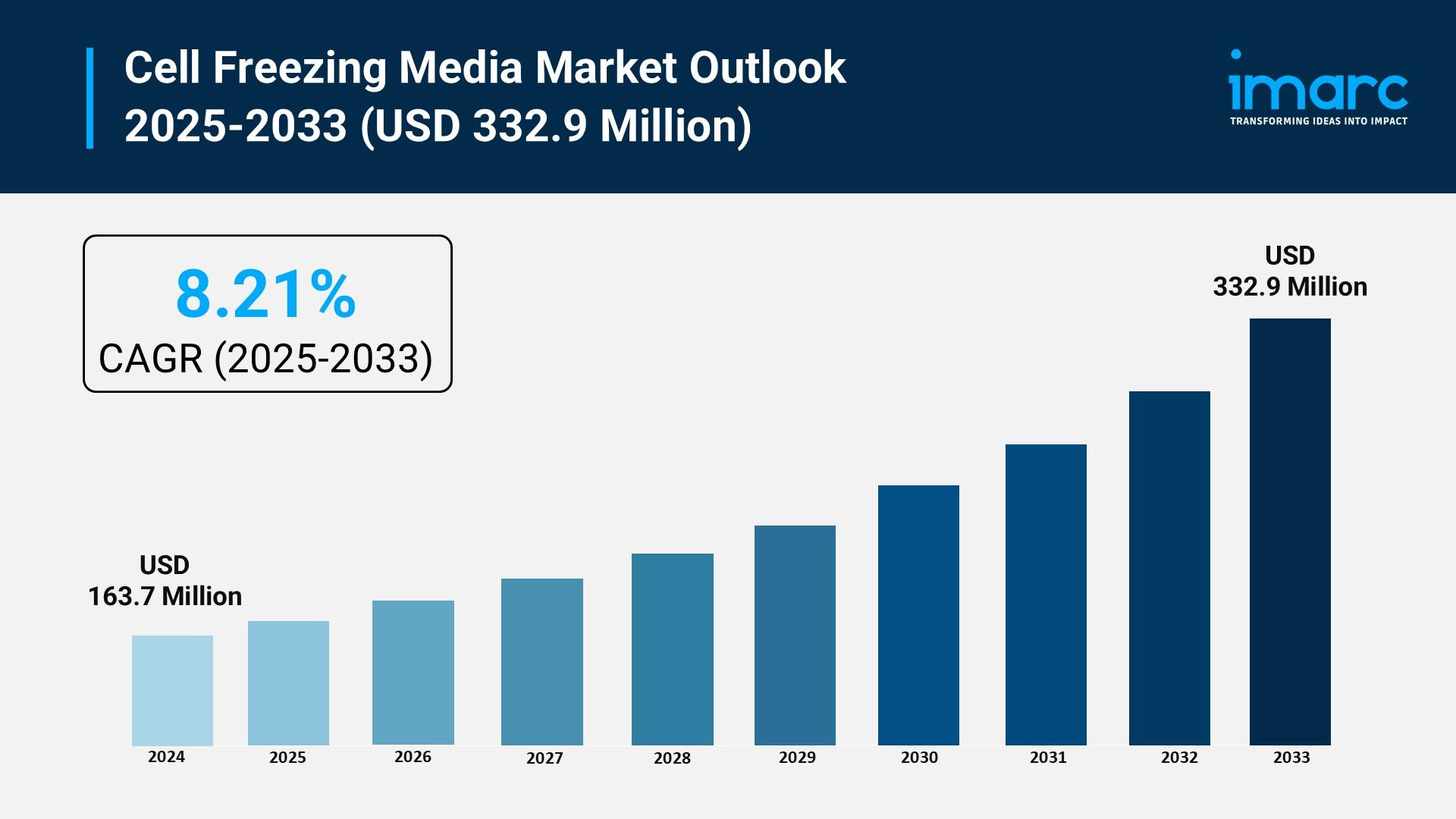

The cell freezing media market is experiencing rapid growth, driven by increasing adoption of cell and gene therapies, rapid expansion of biobanking activities, and growing investment in biopharmaceutical R&D. According to IMARC Group's latest research publication, "Cell Freezing Media Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", The global cell freezing media market size reached USD 163.7 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 332.9 Million by 2033, exhibiting a growth rate (CAGR) of 8.21% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/cell-freezing-media-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends And Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Cell Freezing Media Market

- Increasing Adoption of Cell and Gene Therapies

The global surge in the development and approval of advanced therapy medicinal products (ATMPs) is a primary growth driver for cell freezing media. Cell and gene therapies, such as CAR T-cell treatments, rely on cryopreservation to ensure the long-term viability and logistical feasibility of living cells used as active drug components. For instance, the U.S. Food and Drug Administration is expected to approve numerous new cell and gene therapy medicines annually in the near term, demonstrating the expanding clinical pipeline that requires high-quality, clinical-grade freezing media. These therapies, which frequently use specific cell lines like stem cells or immune cells, necessitate specialized, chemically-defined cryopreservation solutions to maintain high post-thaw cell recovery and function for successful patient treatment. This growth is directly tied to the commercial scaling of these complex, cell-based therapeutic products by pharmaceutical and biotechnology companies.

- Rapid Expansion of Biobanking Activities

The growing number and scale of global biobanks and biorepositories significantly boost demand for cell freezing media. Biobanks are critical infrastructure for storing diverse, high-quality biological specimens—including stem cells, cancer cell lines, and primary cells—for biomedical research, drug discovery, and regenerative medicine applications. The stem cell lines segment, a major application area, accounted for a substantial share of the cell freezing media market revenue in a recent assessment, highlighting its dominance. The proliferation of cord blood banks, public and private tissue repositories, and academic biobanks across North America and Asia Pacific underscores the necessity of reliable cryopreservation consumables. These institutions mandate high-efficacy, validated freezing media to ensure the integrity and functional stability of millions of cell samples stored for decades.

- Growing Investment in Biopharmaceutical R&D

Increased research and development spending by pharmaceutical and biotechnology companies drives the consumption of cell freezing media, particularly in the drug discovery and biologics manufacturing sectors. These industries rely on cryopreserved cell lines for consistent, reproducible in vitro assays, toxicity testing, and large-scale bioproduction, such as manufacturing monoclonal antibodies. The pharmaceutical and biotechnological companies end-user segment is a leading revenue contributor in the market. Furthermore, major corporations are actively introducing new products, such as novel cryopreservation media designed to enhance therapeutic outcomes or all-in-one genetic stability assays to speed up biosafety testing, indicating continuous investment in supporting cell-based research workflows. The sustained flow of capital into these life sciences applications underpins the need for cryoprotective solutions.

Key Trends in the Cell Freezing Media Market

- Shift Towards Chemically-Defined and Xeno-Free Formulations

A major trend is the accelerated industry movement away from traditional, serum-containing freezing media toward chemically-defined (CD) and xeno-free (XF) alternatives. This transition is essential for enhancing the safety, consistency, and regulatory compliance of cell-based products destined for clinical use. XF media eliminates animal-derived components, reducing the risk of pathogen transmission and unwanted immunological responses in patients. For example, a leading cell therapy technology company recently launched a fully synthetic, serum-free, and protein-free cryopreservation medium specifically optimized for pluripotent stem cells. This product addresses a critical need, as these specialized formulations provide superior batch-to-batch consistency and predictable cell viability, which are non-negotiable requirements for Good Manufacturing Practice (GMP) standards in clinical manufacturing processes.

- Development of DMSO-Free Cryoprotectants

The market is witnessing a significant trend in the research and commercialization of dimethyl sulfoxide (DMSO)-free freezing media formulations. While DMSO remains the most widely used cryoprotectant, accounting for a large segment of the market revenue, its known cytotoxicity and associated adverse patient reactions in high-dose clinical applications are driving the search for safer alternatives. Several companies are now marketing proprietary, non-toxic alternatives for cryopreservation, particularly for sensitive cell types like mesenchymal stem cells (MSCs) and various immune cells. This trend is crucial for advancing regenerative medicine and immunotherapy, where high cell dosage and direct patient administration are common. The successful preservation of primary human cells, such as fibroblasts and keratinocytes, for extended periods with retention of functional characteristics using these newer, gentler formulations exemplifies this shift.

- Integration with Automation and High-Throughput Systems

Cell freezing media is increasingly being developed for seamless integration with automated and high-throughput cryopreservation workflows, moving beyond manual benchtop protocols. This trend is vital for supporting the scalability and standardization required by large biobanks, centralized cell manufacturing facilities, and contract research organizations (CROs). For instance, new ready-to-use freezing media solutions are being designed for direct use with automated controlled-rate freezers and robotic liquid-nitrogen storage systems. These automated systems are entering clinical use and minimize human error while ensuring consistent cooling profiles for thousands of samples. The objective is to standardize the entire cryopreservation process, from sample accession to post-thaw recovery, thereby guaranteeing reproducibility, which is a key requirement for international bodies seeking to harmonize protocols across global laboratories.

Leading Companies Operating in the Global Cell Freezing Media Industry:

- AMSBIO

- BioLifeSolutions Inc

- Bio-Techne

- BPS Bioscience, Inc.

- Capricorn Scientific

- Cell Applications Inc.

- Cell Systems (AnaBios Corporation)

- HiMedia Laboratories

- Merck KGaA

- Sartorius AG

- STEMCELL Technologies

- Thermo Fisher Scientific Inc.

Cell Freezing Media Market Report Segmentation:

By Product:

- DMSO

- Glycerol

- Others

DMSO dominates the market share, enhancing cell preservation during cryopreservation, with companies like Thermo Fisher Scientific launching products that ensure high viability.

By Application:

- Stem Cell Lines

- Cancer Cell Lines

- Others

Stem cell lines lead the market value due to their unique ability to self-renew and differentiate, with Lonza introducing ready-to-use cardiac cells for improved research applications.

By End Use:

- Pharmaceutical and Biotechnological Companies

- Research and Academic Institutes

- Others

Pharmaceutical and biotechnological companies represent the largest demand segment, innovating advanced cell freezing media to preserve cell viability, exemplified by new offerings from Merck KGaA.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America holds the largest market revenue share, with comprehensive analysis covering major regions like Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302