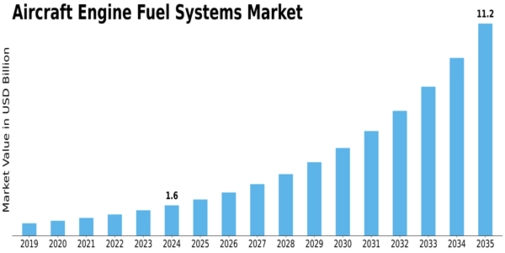

The global aircraft sector is undergoing transformation as airlines and manufacturers strive to meet stricter fuel-efficiency and environmental mandates. At the heart of this transition lies the Aircraft Engine Fuel Systems Market Growth , addressing critical needs such as reliable fuel delivery, monitoring and control. According to MRFR, the market is expected to grow from USD 1.61 billion in 2024 to USD 11.2 billion by 2035, representing a CAGR of 19.3%.

Industry Overview

Fuel systems for aircraft engines encompass components such as pumps, valves, piping, inerting systems, filters, gauges and fuel control monitoring. These systems are fundamental to ensuring that the engine receives the correct amount of fuel under varying operating conditions, maintaining safety, performance and efficiency. As newer engine architectures (jet, turboprop, UAV engines) emerge, the demand for sophisticated fuel systems rises. The overview of the industry reflects a convergence of aerospace engineering, fuel-management software, sensors and regulatory compliance.

In the aerospace & defence domain, the push for lower operational costs and reduced greenhouse-gas emissions is driving manufacturers to invest in advanced fuel system technologies. Moreover, the expansion of commercial aviation in Asia-Pacific and Latin America, alongside growth in military and UAV applications, contributes to growing demand for engine fuel system upgrades and new installations.

Key Players

Major industry participants shaping the market include Honeywell International Inc., Eaton Corporation, Parker Hannifin Corporation, Woodward, Inc., Triumph Group, Inc., Meggitt PLC, GKN PLC, Safran SA and Crane Co. These companies are leveraging their expertise in aerospace systems to develop high-performance fuel systems that address efficiency, weight reduction and reliability.

Segmentation Growth

The report segments the market by engine type (jet engine, helicopter engine, turboprop, UAV engine), by component (inerting systems, piping, valves, pumps, fuel control monitoring systems, filters, gauges), by application (commercial, military, UAV), by technology (pump feed, fuel injection, gravity feed) and by region (North America, Europe, Asia-Pacific, Middle East & Africa, Latin America). Each segment is demonstrating distinct growth patterns: for instance, UAV engine systems are gaining traction as unmanned aerial platforms proliferate, while commercial aviation continues to demand large-scale fuel system deployments.

Outlook Summary

Given the scale of investment, the industry overview clearly points to a vibrant growth phase. As environmental regulations tighten and aircraft designs evolve, the aircraft engine fuel systems market is set to play a pivotal role in the next generation of aviation. Companies with strong R&D, global supply chains and partnerships with OEMs will be best positioned to capitalise on this trend.